The price can go to zero and people like this will still boast about the blockchain continuing to function. They're two different discussion topics: does the technology work, and is it actually worth anything?

The price can go very low and stable coins and DeFi protocols around those can still function exactly as they ever have. A well regulated stable coin will function like any other financial service the West is used to.

A money market fund is federally regulated to be 30% liquid per week.

Because of this, it is very difficult to build a MMF that has much better returns than your competitors. In particular, most MMFs are in-and-around 3.6% APY returns.

These crypto-coins are promising 6%, 10%, 18%, or 20% returns APY. Spoiler alert: they aren't being run like a well regulated MMF.

--------

BTW, a money market fund is a mutual fund with regulations such that 1 share in the MMF is equal to $1. They are the already legal stablecoins you've been looking for.

We can look at the performance of say, VMFXX, which has been $1.00000000 per share for the last 3 or 4 decades. Meanwhile, even the biggest Tether stablecoins floats to $0.998 or $1.001 regularly. Certainly doesn't show very much confidence in the scheme.

This 6% staking or whatever, it's not stable. Never has been, never will be. You can't offer a better rate than the risk free rate unless you are willing to take on risk.

People who want 1 fund == $1 get savings accounts and/or money market funds (depending on their risk tolerance. Savings Accounts are safer but earn less. MMFs have fewer regulations and can therefore offer slightly better rates but for that extra risk).

Anyone promising 7% returns is lying to you. That's far above what even the "riskier" MMFs offer.

-----------

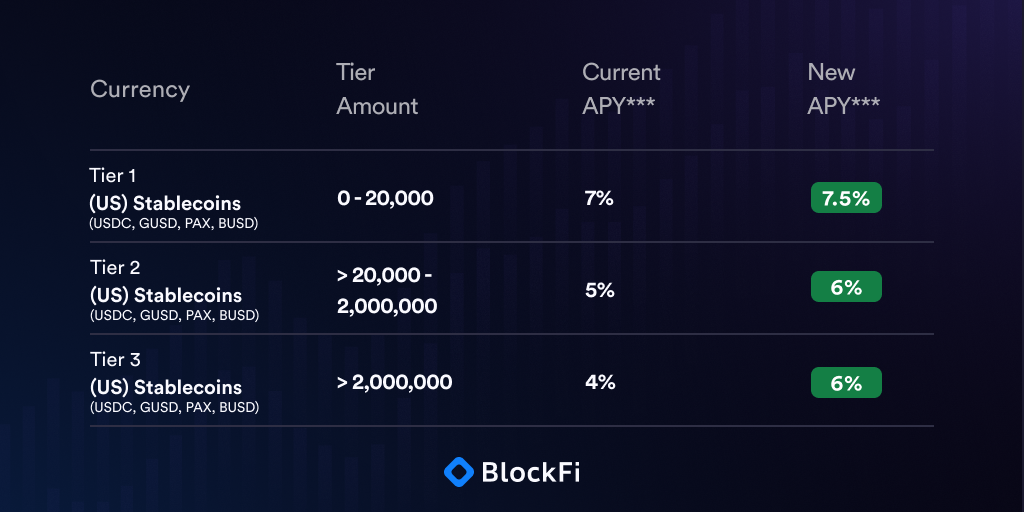

Anyway, USDC is just a really weird bond market, where you end up offering loans (which are called "stakes" for some reason) to shady companies at far below market rates (ex: CCC Debt was 10% APY to 16% APY if you bought it on the open market. But if its "Staking" with BlockFi, it only earns 7%). Instead of thinking if these companies would return their money back, people handed money over-and-over to these other companies and wondered why it didn't come back.

If you really want to lend money to shady companies, I suggest finding rated bonds (even junk bonds) and playing with that instead.

{kind=link}