Reg NMS requires that brokers fulfill orders at the lowest possible rate first. So if an HFT shop sets a trap for you on one exchange (offering 100 stocks a tiny bit cheaper), your broker would have to trade in that first. The HFT would then front-run you to the other exchanges, buy up what it can, and sell it back to you a bit higher. They can do this because they have lower latency. Add dark pools to the mix and the opportunities become even bigger.

This has been pretty thoroughly debunked. I don't really think this ever happened. There is just way too much uncertainty and risk to ever get an edge.

Remember HFT worship at the alter of the law of large numbers, meaning they get a 51% edge and ratchet up the frequency. So a typical strategy might be 48% profitable, 40% wash and 12% unprofitable.

0+ orders on the other hand, now that was a profitable strategy while it lasted:)

Would avidly read the comment adding some detail to this. :)

The book you link to in that comment (_Flash Boys: Not So Fast_) is really fantastic. It strikes me as being written in a style especially congenial to nerd message board people like me: detailed, episodic, point-by-point takedown. It's like a very long Reddit comment, and I mean that in the best way.

Long story short. RegNMS said people have to get the best price for their order. Now in a distributed system, which the US fragmented markets are, you know you can't know for cetain what hte state of the world is.

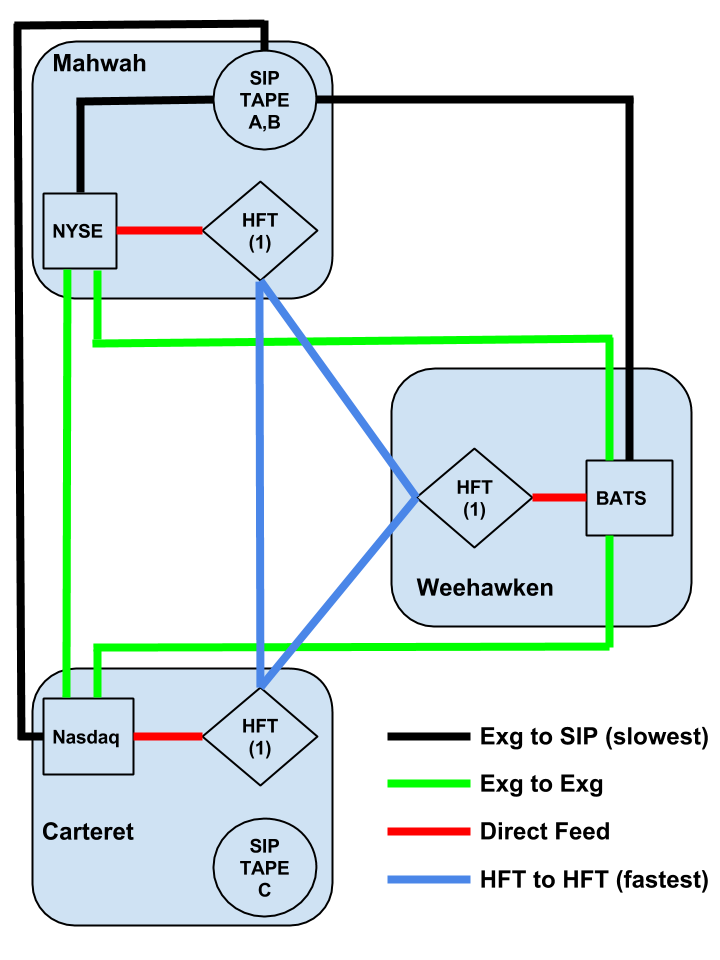

warning simplification ahead

Each market and dark pool has to trade at the price currently listed by the SIP. Now the sip is old and slow. Exchanges offer 2 prices sources,

- the SIP as legally requried

- a direct feed, which serious traders use.

The direct feed is faster, so by the time an exchange (A) reports a trade to another exchange(B) via the sip, the HFT guys who own their own microwave radio lines have notified their computers at exchange B, and moved their orders.

I was curious about microwave radio lines so I did a little digging[1]. It appears that microwave radio can double the speeds of fiber. Though the towers are limited by distance (max ~60mi separation), HFT shops buy/rent microwave tower networks connecting cities. For example, one HFT firm owns a network of ~30 microwave towers connecting NJ to IL that transmit 1.6 ms faster than fiber.

I see your point about the risk, but is there really that much activity in most stocks that getting to the top of the sell pile would be a large enough issue? As I understand some order types were more or less designed to give HFT an edge.

Although I suppose the profits to be made by any strategy dry up pretty quickly as more shops discover it, so it does make sense to me that this doesn't appear to be done any more. I mean, isn't that what worked a few months ago doesn't work any more is the only thing most people posting about HFT can agree about? :D

I have no experience in electronic trading and my knowledge of it mostly comes from HN posts and - as you guessed correctly - Flash Boys, so please forgive my ignorance

> As I understand some order types were more or less designed to give HFT an edge.

And some order types are more or less designed to give large block traders an edge.

Most of the latency game you read about is not getting to trade, its getting the opportunity to cancel your orders. A common misconception is that HFT groups are acting as middle men. They aren't. They are the counter parties on all the exchanges, they are just updating what they are offering faster than others.

Sure. But, after interviewing a bunch of HFT developers over the last 6 months (because: reasons), the understanding I've developed is that "latency arbitrage" --- which is what you seem to be describing --- is no longer particularly profitable, or the focus of what most "HFT firms" do. Is my understanding broken?

No, the market evolved as it always does. But, so much of the "HFT is evil" belief stemmed from the subprime era and with respect to fair play at the time, you can't ignore the impact of NMS. I went back to grad school in 2010 and had to be careful to whom I told my background, else I'd get roped into some morality debate with a 26 year old Occupy activist who didn't know what a market order was.

Nowadays, I really don't see much edge in trading at all.

I would love to know what those traders you've spoken with think is profitable. I see my old bosses at Rom near the CME almost every Friday and I haven't heard a positive line from them in 5+ years.

Latency arbitrage is pretty much impossible as a newcomer and many firms are getting squeezed out of that particular opportunity. Think Jump, KCG, and Citadel...Jump/KCG both share satellites across the US...read more about the radio dish networks here: https://sniperinmahwah.wordpress.com/2014/09/22/hft-in-my-ba...

Simple latency arb strategies are totally an arms race now, with very high barriers to entry. That does not mean however that latency becomes unimportant - if you are a market maker you're essentially playing the same game in reverse - you want to move your quotes out of the way to avoid getting your lunch eaten by those aggressors.

I would argue that the HFT that gets all the negative press are those systems taking advantage of Reg NMS. I think the regulations that caused it should be removed. If you're looking for a black & white definition to satisfy the age old quest to define high frequency trading, you could pick worse.

There are other strategies that get a lot of bad press, of course, but they are not novel with respect to strategy, only speed. Deception is par for the course. And sometimes, products are just poorly designed. Leveraged ETFs, for example.

He could be saying but if so its not true. RegNMS trading is a thing. Latency arbitrage is also a thing. There are also a wide variety of strategies that may exploit the idiosyncrasies of a specific exchange. Multiple venues, while useful and common, are not needed in all HFT strategies.

{kind=link}